S&P 500, Dollar, Fed Forecast, Inflation and NFPs Talking Points:

- The Market Perspective: USDJPY Bearish Below 137; EURUSD Bullish Above 1.0000; Gold Bearish Below 1,750

- Fed Chairman Jerome Powell confirmed that the Fed is likely to downshift its tempo of rate hikes going forward, which should not have been a surprise, but it was an equity catalyst

- While the S&P 500 jumped its tight range and 200-day SMA, the Dollar was noticeably more reserved in its retreat – the PCE deflator ahead could materially change that backdrop

Discover what kind of forex trader you are

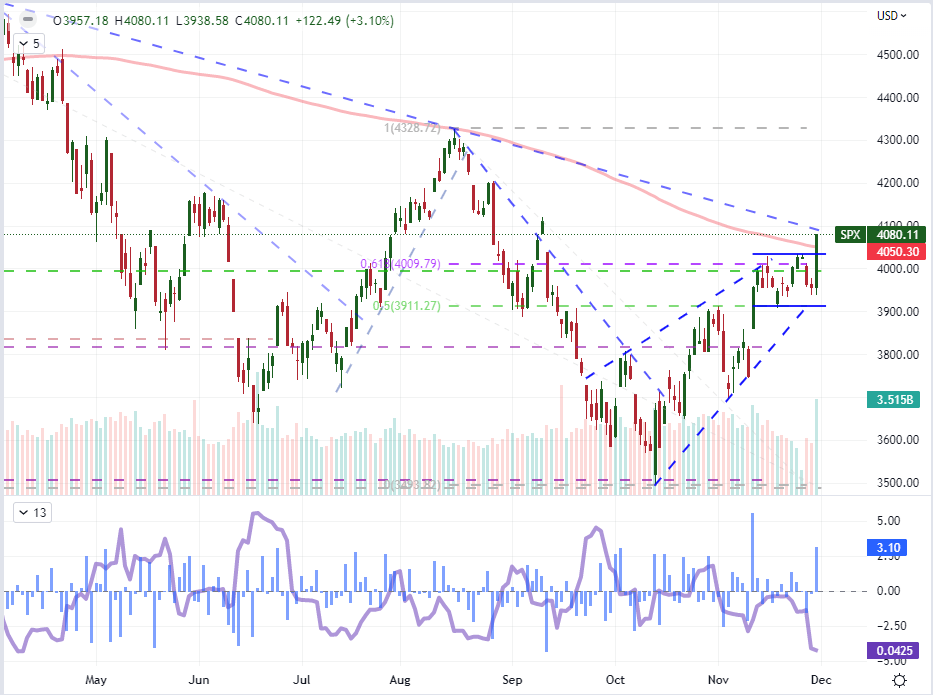

It has finally happened: the narrow range on benchmark risk assets was finally cleared in the afternoon hours of this past US trading session. The technical milestone was as unmistakable as the fundamental catalyst that sparked the move. At 18:30 GMT, the US indices started a charge higher on comments from Fed Chairman Jerome Powell that support something that has been insinuated in different venues (economist observations, trader speculation and even other Fed officials’ remarks) that a moderation in the pace of rate hikes was close at hand. While this has been the leading expectation for the FOMC’s course moving forward for some weeks, the market nevertheless decided to interpret the echo as a rally call for the bulls. Not only did the S&P 500 managed to clear the 3.2 percent range it had trekked out the past 12 trading days, but it would go on to clear the 200-day moving average (first time since April 7th) and ultimately post its second largest daily rally (3.1 percent) since May of 2020. There are further technical barriers overhead, but the fundamental charge behind this move should draw serious scrutiny for those looking for the kind of conviction that would restore us to a long-term bull market.

Chart of the S&P 500 with 200-Day SMAs, 13-Day Range and 1-Day ROC (Daily)

Chart Created on Tradingview Platform

What exactly was it that charge US indices to rally – and the Dow Jones Industrial Average to overtake the 20 percent advance from its September low milestone, marking a technical ‘bull market’? There was both a prepared statement and separate remarks offered by Chairman Powell. The comment that seemed to capture the market’s interest was that the time to slow the pace of rate hikes was soon at hand and could begin as early as December. While that same view was insinuated by a number of Fed officials in previous days and weeks – some saying it explicitly – the market was motivated by the affirmation. In practical terms, the probability that the central bank hikes 50 basis points at the meeting on December 14th ended the day at 76 percent according to Fed Funds futures….exactly the same level it was a week ago. Another restatement made by Powell during his prepared remarks was that the path of rate hikes would be higher than was projected in the September Summary of Economic Projections and they would need to be kept at ‘restrictive’ levels for ‘some time’. So rate forecasts are still seen as remarkably restrictive and the threat of recession still hangs prominently in the background, but appetites seemed to dictate the priority of the insights.

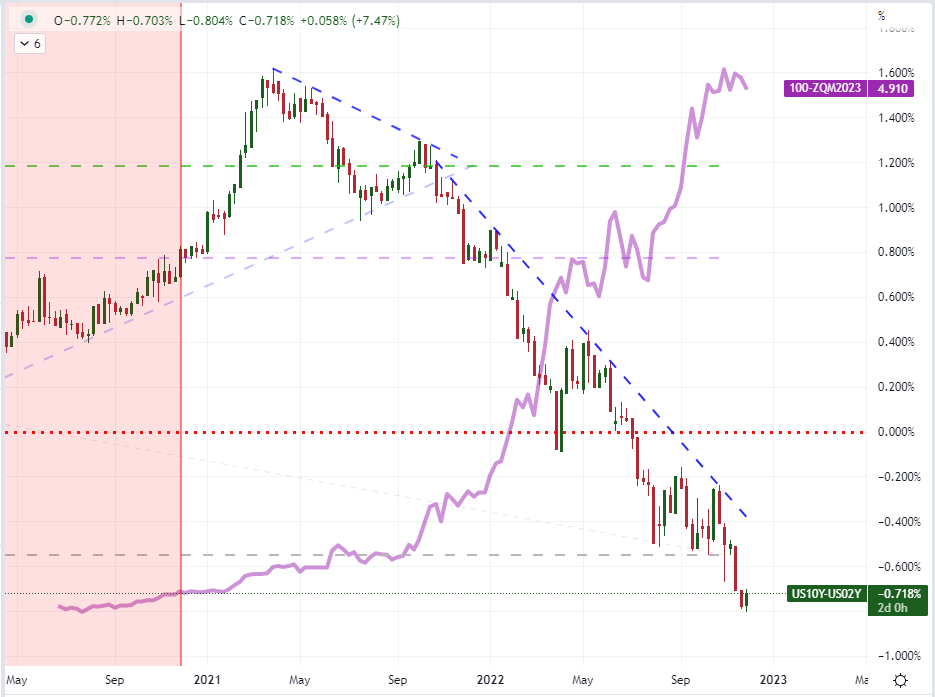

Chart of the US 10-Year to 2-Year Yield Spread Overlaid with the Implied Jun 2023 Fed Rate (Daily)

Chart Created on Tradingview Platform

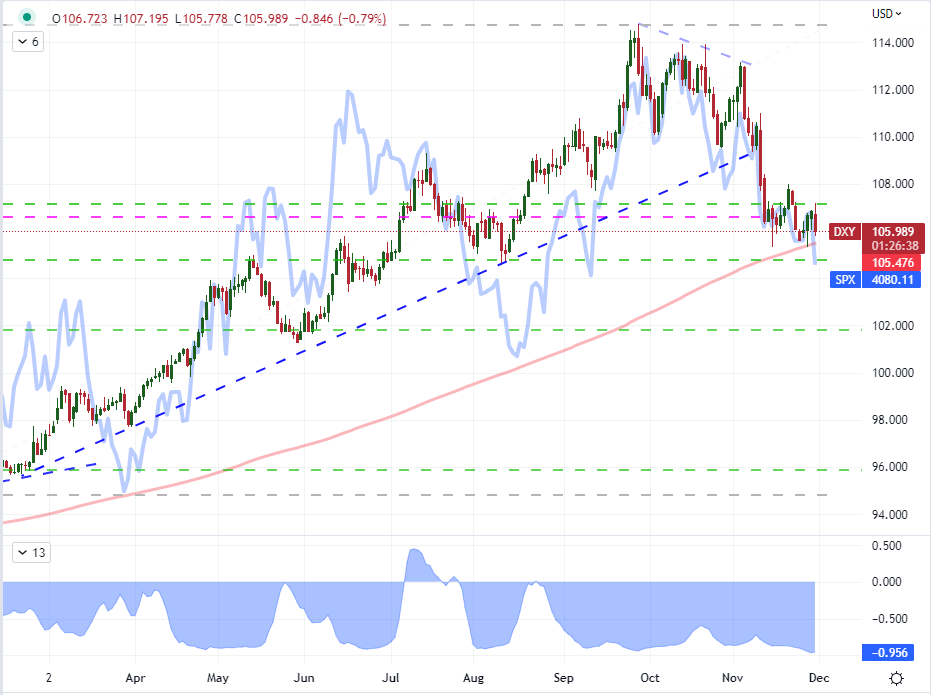

Markets have been extremely constricted over the past few weeks, that breakout pressure was set very high. Resolution from such narrow trading bands can come in two forms: a break of ‘necessity’ whereby it resolves without a distinct fundamental motivation or one of ‘conviction’. There was certainly a distinct even around for the traction, but the implications of the update don’t exactly reflect the enthusiasm measured in the market. A sanity check to this fundamental dubiety can be assessed in the performance of the US Dollar. While the DXY Index did slip on the day, it wouldn’t break its own range and 200-day SMA support as a mirror to the US index. To gauge how unusual that is, we look at the correlation between the two benchmarks below. I overlaid an inverted S&P 500 to give a visual comparison; but it is the 20-day rolling correlation that really signals how significant the deviation. Over the past month, the relationship between USD and SPX has been -0.96. A -1.0 reading would indicate they moved in a perfect mirror of each other.

Recommended by John Kicklighter

How to Trade USD/JPY

Chart of the DXY Dollar Index Overlaid with Inverted S&P 500 with 20-Day Correlation (Daily)

Chart Created on Tradingview Platform

While I have concerns over the fundamental backing to the capital market’s relief rally, it is still possible to keep the expansion of volatility pointed in favor of the bulls. One of the most influential catalysts to extend the suspension of disbelief is Thursday’s top economic listing: the US PCE deflator. As innocuous as this indicator’s name may be, it is the Federal Reserve’s favorite inflation indicator. We saw what happened after the US CPI came in softer than was expected back on November 10th: the Dollar broke its bull trend and the S&P 500 posted an incredible 5.5 percent rally. Despite the central bank’s preference, the market hasn’t really treated this series with the same level of respect through repricing. Yet, if the data point reinforces the bullish sentiment from the less hawkish forecast; it may see its status elevated owing to the convenience. Further, if the PCE is ‘favorable’ it could warp the response scenarios of the NFPs to be interpreted positively despite the outcome: a strong reading registered as evidence of avoiding a recession while a weak one further pressuring the Fed to throttle back hikes.

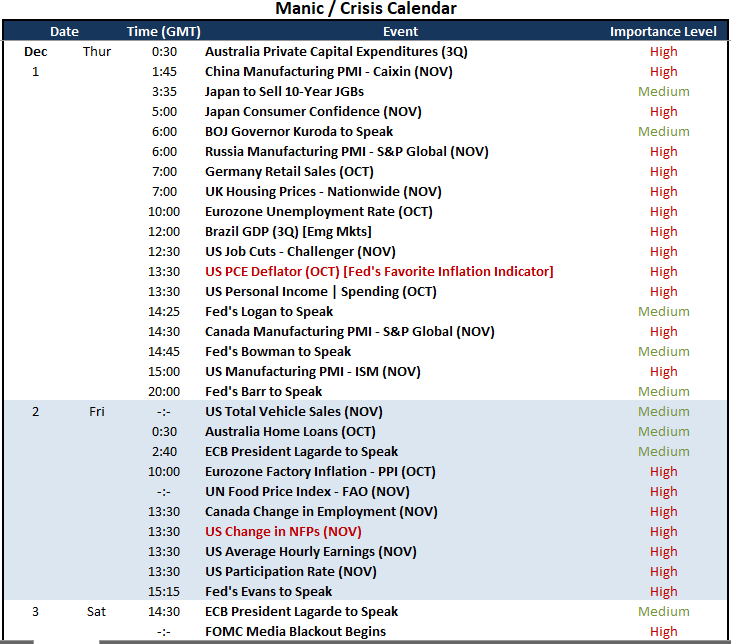

Critical Macro Event Risk on Global Economic Calendar for the Next 48 Hours

Calendar Created by John Kicklighter

Trade Smarter – Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Subscribe to Newsletter